Buying Where Short-Term Rental Permits Are Capped: 2025 Guide to Value, Loans, and Cash Flow

In many cities, short-term rental permits are scarce, non-transferable, or frozen. Here’s how capped permits change home values, mortgage approvals, and cash flow math for buyers in 2025.

- Permit scarcity can add or remove six figures of value; comps must match permit status, not just bedroom count.

- Lenders now verify permit eligibility, insurance, and HOA rules; DSCR and second-home loans treat STR income differently.

- Model a fallback plan: if the permit is lost or delayed, long-term rent must cover debt, taxes, and rising insurance.

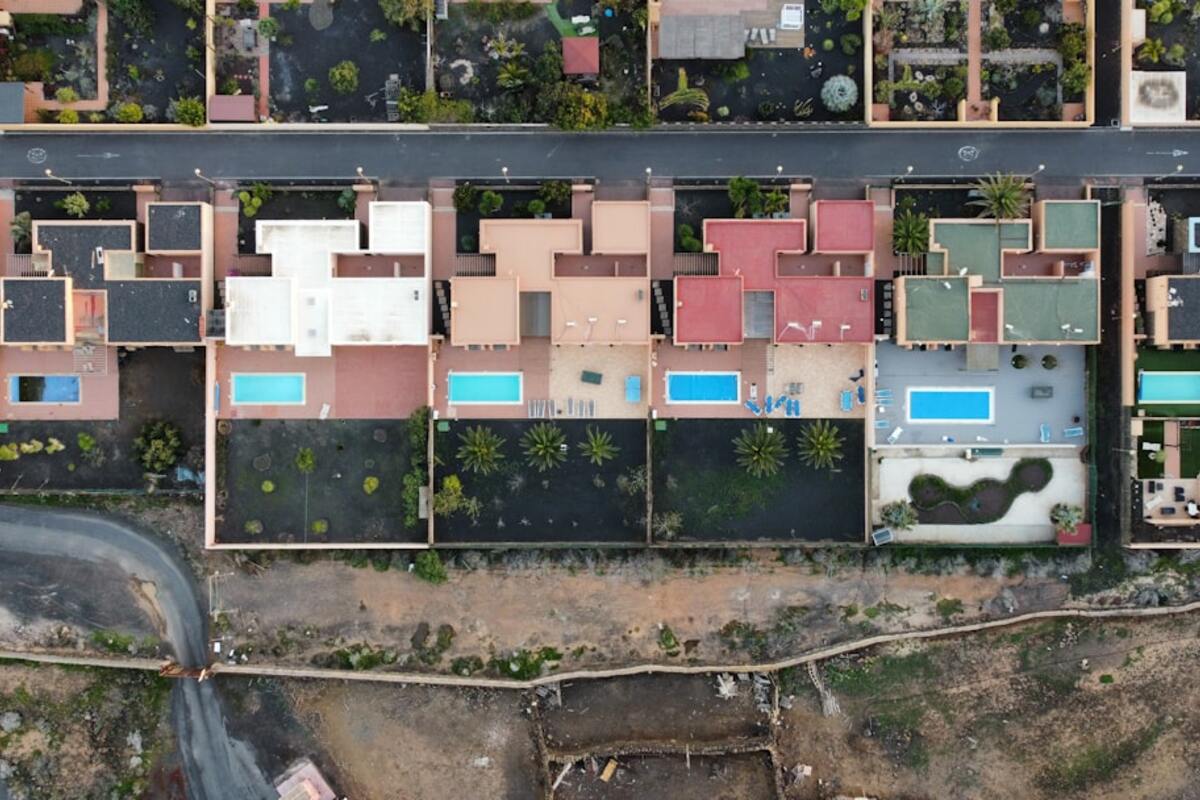

Short-term rentals have matured from a side hustle into a regulated property class. In 2025, dozens of popular markets now cap the number of permits, restrict non-owner-occupied units, and tie permits to the owner rather than the address. That shift re-prices homes: two nearly identical houses on the same block can trade at very different numbers depending on whether they carry an active short-term rental (STR) permit that actually survives a resale.

For buyers, the headline question is no longer just nightly rates and occupancy. It’s the permit: does it exist, does it transfer, and is the property genuinely eligible under today’s rules, not last year’s? Downstream, lenders, appraisers, title companies, and insurers are building these answers into approvals. To keep deals on track, you’ll need to verify policy and paperwork early, model downside scenarios, and write offers that account for regulatory timing.

How Permit Caps Change What a Property Is Worth

Permit caps don’t merely change operating rules—they redefine the type of asset you are buying. A home that can be lawfully operated as an STR with no new approvals is effectively a different property than the same home that must wait on a citywide lottery. Appraisers are catching up by using permit-status-matched comparables where market data allows it, and buyers should, too.

Here are the key dimensions that tend to move price most in capped markets:

- Transferability: Whether the STR authorization runs with the owner, with the address, or not at all after sale.

- Cap ratio and waitlist: Size of the cap relative to housing stock, and whether a waitlist exists or is frozen.

- Hosted vs. unhosted: Many cities allow hosted stays (owner present) but prohibit non-owner-occupied stays.

- Zoning overlays: Some neighborhoods or coastal zones are carved out for stricter or looser rules.

- Compliance track record: Known violations can trigger cooling-off periods or make permits unrenewable.

When you evaluate comps, force-match these traits. If your subject is a non-owner-occupied townhouse with a transferable permit, a comp that needs the owner to live on-site is not truly comparable, even if the square footage aligns.

| Permit scenario (2025) | Transfer on sale | Cap status | Typical value impact | Lender perspective |

|---|---|---|---|---|

| Non-owner-occupied STR in tourist overlay | Yes (address-bound) | Within cap; renewals prioritized | Premium vs. non-eligible homes (often 8–20%) | Accepts documented permit as ongoing income source |

| Hosted-only permit | No (owner-bound) | Cap irrelevant to hosted stays | Smaller premium; depends on owner occupancy plan | Second-home underwriting; limited income consideration |

| Lottery/waitlist required | N/A | Cap met; no new permits | Discount vs. fully permitted peers; price to long-term rent | Income excluded; stress to MTR/LTR fallback |

| HOA bans STR regardless of city rules | N/A | Not applicable | STR premium erased; HOA comps control | Must underwrite as primary/second home or LTR only |

Because permit caps are hyperlocal, even small boundary changes can swing value. Call the planning office to confirm a parcel’s exact overlay and whether the permit refers to the owner, the address, or the business entity. If a listing claims “permit in place,” ask for the permit number, renewal date, and any outstanding compliance items. One overdue occupancy tax filing can derail a renewal and crater the pricing you offered.

Investors should also map neighborhood sentiment. In many cities, the enforcement budget follows 311 noise calls. If council districts are considering tighter caps, a permit that looks safe on paper can be a melting ice cube. Price that risk by asking what the exit looks like if STR use narrows to 30 or 60 nights per year or is limited to hosted stays only.

What Lenders Check in 2025

Lenders in 2025 don’t assume STR revenue unless they can verify that you can legally operate. The degree of scrutiny depends on the loan product, and the rules differ sharply between second-home, conventional investment, and DSCR programs.

Common checkpoints you should expect during underwriting:

- Permit verification: A copy of the active permit or a municipal email/portal printout showing transferability and renewal requirements.

- Zoning and HOA confirmation: Clear evidence there’s no conflict between municipal code, CC&Rs, and building rules.

- Insurance match: A policy that explicitly covers short-term rental activity, not a standard landlord or homeowners form.

- Tax compliance: Proof that prior owners remitted occupancy taxes if a transfer depends on a clean ledger.

- Income evidence: Actual trailing 12 months (T-12) from platform statements, bank deposits, and a third-party market report if there’s limited history.

Underwriting flavors by loan type:

Conventional investment loans: Most agency lenders will not count projected Airbnb income without a transferable permit and history. They may allow long-term rent from an appraiser’s market rent schedule but ignore nightly revenue, pushing buyers to qualify on W-2 income or long-term leases.

Second-home loans: Lenders generally do not rely on STR income at all. They will scrutinize occupancy intentions and can deny loans if marketing materials show an obvious investment focus. Insurance must still match actual use.

DSCR loans: Debt-Service Coverage Ratio programs are built for rental income, and many now accept STRs using a blend of T-12 actuals and independent market projections. Expect minimum DSCR thresholds around 1.05–1.20 for short-term rentals, with rate add-ons for non-occupied STRs. Some DSCR lenders require evidence that the permit is either transferable or already in the borrower’s name before closing.

Red flags that commonly stall closings:

- Listing says “grandfathered permit,” but city code shows grandfathering ends at sale.

- HOA allows “30-day minimum” stays, which is incompatible with nightly rentals.

- Insurance binder excludes business activity or occupancy under 30 days.

- Seller used multiple platforms but never registered for occupancy tax, prompting a compliance hold.

Get ahead by building a “closing folder” early: permit documents, code citations with highlighted clauses, HOA letters, an insurance quote that names STR use, and a T-12 with matching bank statements. Share this with your lender and appraiser before the inspection window closes.

Cash Flow Modeling Under Permit Uncertainty

With caps and crackdowns, the winning approach is a two-path model: a base case where permits and calendars perform as expected, and a fallback case where you operate as a mid-term rental (MTR) or long-term rental (LTR). If both paths produce acceptable returns, the property can withstand policy shifts.

Build your model in layers:

- Gross revenue: Blend seasonality, city event spikes, and minimum-stay rules. Keep platform delist days for compliance inspections.

- Operating costs: Cleaning, consumables, dynamic pricing software, permit fees, occupancy taxes, and a reserve for complaints or fines.

- Fixed costs: Mortgage PITI, STR insurance, utilities, landscaping, pest control, and internet.

- Regulatory buffer: A 10–20% revenue haircut to reflect permit risk, plus a reserve for fee increases.

Then create a fallback view:

- Mid-term rental (30–90 days): Many caps don’t apply to 30+ day stays. Price against travel nurses, corporate housing, and insurance placement demand.

- Long-term rental (12 months): Price a conservative rent with a 5–10% vacancy factor and landlord-friendly insurance.

- Exit options: If cap rules tighten, can you sell into a hosted-only buyer pool or to an owner-occupant at a strong price per square foot?

Run simple stress tests to avoid rosy spreadsheets:

| Stress lever | Change | Impact to DSCR | Mitigation |

|---|---|---|---|

| Occupancy drops | -10 percentage points | -0.10 to -0.20 DSCR | Pivot to MTR; lower cleaning cost cadence |

| Insurance jump | +25% premium | -0.03 to -0.06 DSCR | Higher deductible; STR-specific carriers |

| Permit delay | 90 days post-close | No STR income in Q1 | Bridge cash reserve; initial MTR placement |

Because occupancy taxes and remittance software fees can add 5–15% to top line, model them explicitly instead of burying them in “miscellaneous.” Many cities partner with compliance vendors that bill per listing; include that subscription in your monthly burn.

Offer and closing checklist to keep your downside covered:

- Make the offer contingent on written verification of permit transfer or new issuance eligibility.

- Require seller to cure any occupancy tax arrears and code violations pre-close.

- Ask the appraiser to cite permit status in the report and to use permit-alike comps where available.

- Bind STR insurance before closing with accurate use and occupancy limits.

- Pre-sell your fallback plan to the lender: sample MTR lease comps or a signed corporate housing inquiry list.

Design choices also matter for regulators and neighbors. Think acoustics and parking: a well-placed sound monitor, clear house rules, and trash-day reminders reduce complaint risk that can otherwise jeopardize renewals. Many cities run point-based systems where repeat noise or trash violations can suspend your permit even if you’re below the cap.

Data sources to make fast, accurate calls:

- Municipal code portal and clerk’s office minutes for pending amendments.

- Planning/GIS map to confirm overlay boundaries for your parcel ID.

- STR platforms’ city pages summarizing local rules (cross-verify with actual code).

- HOA/COA document packages and board meeting notes for evolving building rules.

- Local hospitality demand data (event calendars, seasonal ADR swings).

It depends on the city. Some permits are address-bound and transfer at sale if the application is timely; others are owner-bound and expire upon transfer, requiring the buyer to reapply under a cap. A minority of markets have frozen new permits entirely; in those, sales do not carry STR rights unless the code explicitly grandfathered address-bound permits.

It depends on the city. Some permits are address-bound and transfer at sale if the application is timely; others are owner-bound and expire upon transfer, requiring the buyer to reapply under a cap. A minority of markets have frozen new permits entirely; in those, sales do not carry STR rights unless the code explicitly grandfathered address-bound permits.

Conventional and second-home loans generally won’t count projected nightly revenue unless there is a transferable permit and trailing history. DSCR lenders are more flexible and can use a blend of actuals and third-party market reports, but they still require legal eligibility and insurance appropriate for STR use.

Conventional and second-home loans generally won’t count projected nightly revenue unless there is a transferable permit and trailing history. DSCR lenders are more flexible and can use a blend of actuals and third-party market reports, but they still require legal eligibility and insurance appropriate for STR use.

Use an addendum making the deal contingent on issuance or transfer of the permit, with a right to cancel if a moratorium or lottery prevents operation. Keep a fallback underwriting path—mid-term or long-term rent—so the deal can still close if you love the property’s fundamentals.

Use an addendum making the deal contingent on issuance or transfer of the permit, with a right to cancel if a moratorium or lottery prevents operation. Keep a fallback underwriting path—mid-term or long-term rent—so the deal can still close if you love the property’s fundamentals.

Most standard homeowners and landlord policies exclude business activity or stays under 30 days. You’ll likely need a dedicated STR policy, sometimes combined with commercial general liability. Expect higher premiums in coastal and wildfire zones, and be ready to document smoke/CO detectors, egress, and safety features to secure coverage.

Most standard homeowners and landlord policies exclude business activity or stays under 30 days. You’ll likely need a dedicated STR policy, sometimes combined with commercial general liability. Expect higher premiums in coastal and wildfire zones, and be ready to document smoke/CO detectors, egress, and safety features to secure coverage.

In capped cities, the best deals reward preparation. Treat the permit like a title document, not a marketing bullet. Price to the rules that will govern you on Day 1 of ownership, verify them in writing, and make sure two paths—STR and MTR/LTR—can both pay the bills if the wind shifts. Where the permit is durable and transferable, you can justify paying up. Where it’s sticky, fragile, or owner-bound, bid with your fallback math and protect yourself with the right contingencies.